Understanding Home Equity Loan Rates:

Home equity loans have long been a popular financial tool for homeowners seeking to leverage their property’s value for various needs, whether it’s home improvements, debt consolidation, or major expenses. One of the critical factors influencing the decision to take out a home equity loan is the interest rate, which can significantly impact the overall cost of the loan. This article will delve into the intricacies of home equity loan rates, factors influencing them, and tips for securing the best rate.

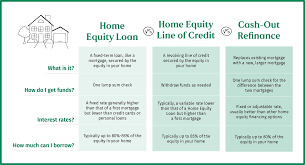

What is a Home Equity Loan?

A home equity loan allows homeowners to borrow against the equity they have built in their property. Equity is the difference between the current market value of the home and the outstanding mortgage balance. Home equity loans are typically offered as a lump-sum amount with a fixed interest rate and a predetermined repayment period. This fixed-rate structure provides stability, as monthly payments remain consistent throughout the life of the loan.

Factors Influencing Home Equity Loan Rates:

One of the most significant factors influencing home equity loan rates is the borrower’s credit score. Lenders use credit scores to gauge the risk associated with lending money. A higher credit score generally leads to lower interest rates because it indicates a lower risk of default. Conversely, a lower credit score may result in higher rates or even difficulty in securing a loan.

2. Loan-to-Value Ratio (LTV):

The loan-to-value ratio is another crucial factor. It is calculated by dividing the amount of the loan by the appraised value of the home. Lenders prefer a lower LTV ratio as it signifies less risk. For example, if you have a home worth $300,000 and are borrowing $60,000, your LTV ratio is 20%. Typically, an LTV ratio below 80% is considered favorable and may result in better interest rates.

3. Market Conditions:

Interest rates are also influenced by broader economic conditions. The Federal Reserve’s policies, inflation rates, and overall economic health play a significant role in determining interest rates. When the Federal Reserve raises or lowers its benchmark rates, it can affect the rates offered by lenders. In a low-interest-rate environment, home equity loan rates are generally lower, and vice versa.

4. Loan Term:

The term of the loan, or the length of time you have to repay it, can impact the interest rate. Shorter loan terms often come with lower interest rates because they present less risk to lenders. Conversely, longer loan terms might have higher rates due to the increased risk over an extended period.

5. Lender Policies:

Different lenders have varying policies and criteria for setting home equity loan rates. Some lenders may offer promotional rates or discounts, while others may have stricter requirements. It’s essential to shop around and compare offers from multiple lenders to find the best rate for your situation.

Current Average Rates:

As of mid-2024, average home equity loan rates are typically between 6% and 8%. However, these rates can fluctuate based on the factors mentioned above. It’s crucial to check current rates with individual lenders and consider your financial situation to get a more accurate picture of what you might expect.

How to Secure the Best Home Equity Loan Rate:

1. Improve Your Credit Score:

Before applying for a home equity loan, take steps to improve your credit score. Pay down existing debts, make timely payments, and check your credit report for errors. A higher credit score can help you secure a lower interest rate.

2. Increase Your Home’s Equity:

Building more equity in your home can result in a lower LTV ratio and better loan terms. Consider paying down your mortgage faster or making home improvements that increase your property’s value.

3. Compare Lenders:

Don’t settle for the first offer you receive. Shop around and compare rates from various lenders, including banks, credit unions, and online lenders. Pay attention to additional fees and terms, as these can affect the overall cost of the loan.

4. Consider Fixed vs. Variable Rates:

Understanding home equity loan typically offer fixed interest rates, which provide predictable monthly payments. However, some lenders may offer variable-rate home equity lines of credit (HELOCs), which can start with lower rates but fluctuate over time. Assess your financial stability and risk tolerance when choosing between fixed and variable rates.

5. Negotiate Terms:

Don’t hesitate to negotiate with lenders. Sometimes, lenders may be willing to offer better terms or reduce fees to secure your business. Ask about any available discounts or promotions.

Conclusion:

Understanding home equity loan rates is crucial for making informed financial decisions. By considering factors such as credit score, LTV ratio, market conditions, loan terms, and lender policies, you can better navigate the process and secure a favorable rate. Always shop around, compare offers, and take steps to improve your financial standing to get the best possible deal. With the right approach, a home equity loan can be a valuable tool for managing finances and achieving your goals.